In the second quarter of 2017, Consumer Enforcement Watch tracked 40 enforcement actions taken against consumer financial service providers. This represents a marginal decrease from the 46 enforcement actions taken against consumer financial service providers that we tracked last quarter, and from the 46 enforcement actions tracked in the second quarter of 2016.

var divElement = document.getElementById(‘viz1504627828947’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’548px’;vizElement.style.height=’858px’; var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

Eighteen of the Q2 2017 enforcement actions were settlements (with or without consent orders), while the remaining actions were court judgments, new actions, and new activity in ongoing enforcement actions.

var divElement = document.getElementById(‘viz1504627912150’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’548px’;vizElement.style.height=’858px’; var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

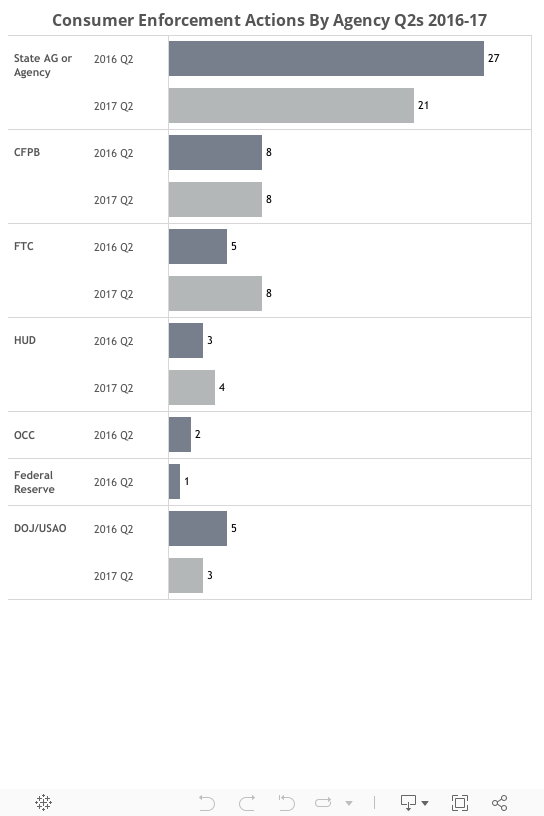

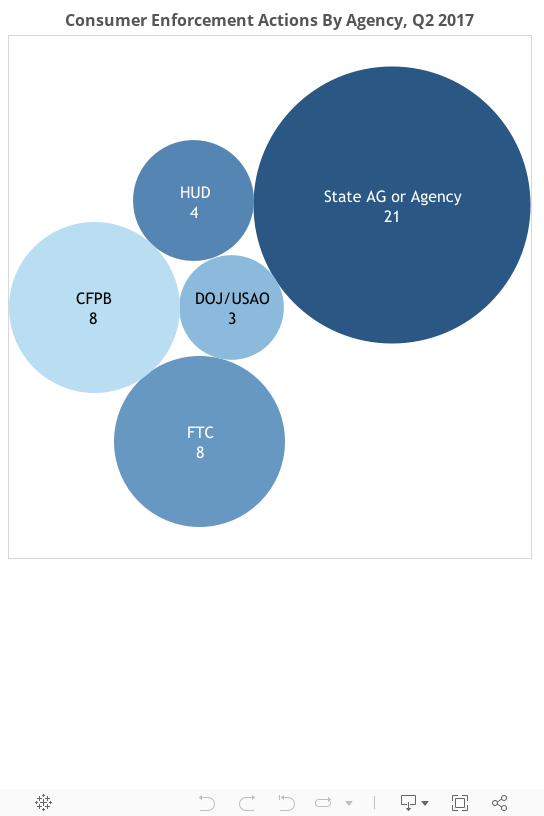

In Q2 2017, state attorney generals and state enforcement agencies were involved in the majority of enforcement actions, accounting for just over half of the enforcement actions tracked—or 21 of the 40 enforcement actions. This number represents a considerable increase from the 11 state enforcement actions we tracked last quarter, and a slight decrease from the 26 state enforcement actions we tracked in Q2 of last year. This quarters’ decline in state enforcement actions relative to the second quarter of 2016 is consistent with the general trend observed last year of declining state activity. However, as overall enforcement actions taken against consumer financial service providers trend downwards, state enforcement actions are representing a greater percentage of the overall pie of activity.

The Consumer Financial Protection Bureau (CFPB) remained the most active federal agency this quarter, accounting for eight actions tracked, although the Federal Trade Commission (FTC) was equally active in Q2. The increase in FTC actions and Department of Housing and Urban Development (HUD) actions in Q2 2017 relative to Q2 2016 is noteworthy considering the overall drop in enforcement actions since last year. Three of the FTC actions were brought in conjunction with the Florida Attorney General, who was particularly active in Q2, accounting for 6 of the 21 state enforcement actions.

In Q2 2017, 24 out of the 40 of the enforcement actions tracked were new or existing litigations. The most highly targeted defendants were mortgage servicers and mortgage originators (10), followed closely by debt collectors and debt settlors (9). Agencies also pursued a number of actions surrounding personal and student lending (6) and auto lending (4).

Corresponding with the CFPB’s continued activity, the Consumer Financial Protection Act (CFPA) remained the statute most frequently at issue in Q2 actions, cited eight times in litigations targeting credit repair services, mortgage servicers, debt collectors, and auto and student lending services. Corresponding with the FTC’s activity, both the Fair Debt Collection Practices Act (FDCPA) (5) and the Federal Trade Commission Act (6) were also frequently invoked.

Federal and state actions resulted in approximately $35 million in civil penalties and settlement payments this quarter, which is just a fraction of the $1.5 billion in civil penalties and settlement payments from Q2 2016, and a substantial decrease in the civil penalties and settlement payments from Q1 2017 ($667.1 million), Q1 2016 ($300 million), and Q3 2016 ($300 million). The bulk of the civil penalties issued this quarter (over $20 million) were collected from a mortgage relief law firm relating to alleged violations of the Mortgage Assistance Relief Services Rule (MARS Rule) and the CFPA.

Enforcement agencies also collected approximately $154.5 million in restitution, consumer relief or disgorgement. This amount is also a fraction of the relief provided to consumers in Q1 2017 ($508.6 million) and in Q1 2016 ($750 million), but more on par with the relief provided to consumers in Q3 2016 ($100 million). Notably that relief includes the $89 million settlement between the Department of Justice (DOJ) and a company engaged in reverse mortgage servicing, in connection with the company’s participation in HUD’s Home Equity Conversion Mortgage (HECM) program, which offers senior citizens reverse mortgages insured by the Federal Housing Administration.

Consumer Finance Enforcement Watch will continue to post quarterly and annually on trends in consumer finance enforcement activity. For specific questions regarding trends by enforcers, industry, or other data, please feel free to contact Kyle Tayman, Levi Swank, or Matt Riffee.