For the second quarter of 2016, Consumer Enforcement Watch tracked 46 enforcement actions taken against consumer finance providers. This represents a slight decrease from the 50 enforcement actions that were tracked last quarter, and a decrease from the 56 actions that we tracked in the second quarter of 2015. Approximately two-thirds of Q2 enforcement actions were settlements (with or without consent orders), with the remainder resulting from court judgments, non-judgment court rulings, and new activity in ongoing enforcement actions.

For the second quarter of 2016, Consumer Enforcement Watch tracked 46 enforcement actions taken against consumer finance providers. This represents a slight decrease from the 50 enforcement actions that were tracked last quarter, and a decrease from the 56 actions that we tracked in the second quarter of 2015. Approximately two-thirds of Q2 enforcement actions were settlements (with or without consent orders), with the remainder resulting from court judgments, non-judgment court rulings, and new activity in ongoing enforcement actions.

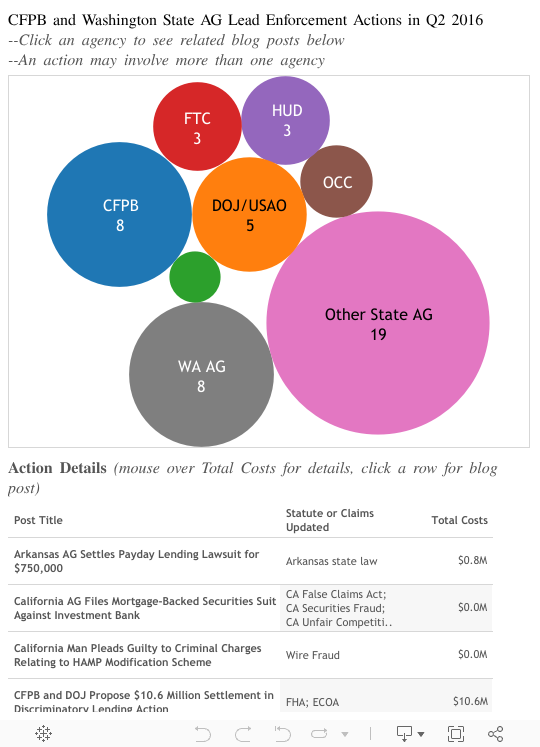

State attorneys general and state regulatory agencies were slightly more active than they were last quarter, bringing 26 of the 46 enforcement actions. The Washington Attorney General was particularly active in Q2, having brought 7 actions related to student lending and one related to debt settlement. Unsurprisingly, and consistent with 2015 trends and Q1 2016, the CFPB remains the most active federal agency, initiating 7 enforcement actions on its own and another action jointly with the Department of Justice. Corresponding with the CFPB’s activity, the Consumer Financial Protection Act (7) was the statute most frequently invoked in Q2. Agencies also pursued actions under the False Claims Act (4), Fair Debt Collection Practices Act (4), Federal Trade Commission Act (3), and Fair Housing Act (3).

var divElement = document.getElementById(‘viz1477339572913’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’544px’;vizElement.style.height=’789px’; var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

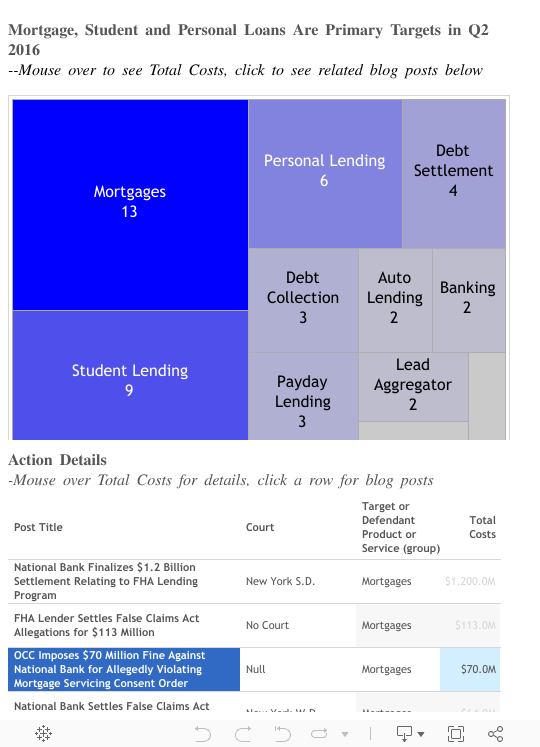

Mortgages were again the primary enforcement target, with 13 mortgage-related enforcement actions in Q2. This is one less action than the previous quarter. Mortgages remain on pace for approximately 54 enforcement actions in 2016, compared to the 68 mortgage-related actions we tracked in 2015. The second quarter also saw substantial enforcement activity in personal lending, with agencies bringing 9 such actions. While enforcement related to debt settlement (4), debt collection (3), and auto lending (2) are all slightly down from last quarter, the number of student lending actions has more than doubled (from 4 actions in Q1 to 9 actions in Q2). This quarter also saw the first credit card-related action in 2016.

var divElement = document.getElementById(‘viz1477339451498’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’544px’;vizElement.style.height=’789px’; var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

Federal and state actions resulted in just under $1.5 billion in civil penalties and settlement payments this quarter. Nearly all of this figure is attributable to just three False Claims Act settlements. The U.S. Department of Housing and Urban Development and Department of Justice secured a $1.2 billion settlement against a national mortgage lender in an enforcement action related to the Federal Housing Administration Direct Endorsement Lender Program FHA-insured loans, and two other similar settlements against FHA mortgage lenders for $113 million and $64 million.

Enforcement agencies also collected approximately $31 million in consumer relief or restitution, which is just a fraction of the $750 million of such relief that Enforcement Watch tracked in Q1. Notably that relief includes actions requiring two online payday lenders to refund $9 million to North Carolina consumers, and actions requiring several national lenders to pay $8 million in restitution to Colorado consumers.

Consumer Finance Enforcement Watch will continue to post quarterly and annually on trends in consumer finance enforcement activity. For specific questions regarding trends by enforcers, industry, or other data, please feel free to contact Kyle Tayman or Joseph Robbins.